By Tommy Wilkes

The European Union and Britain announced new sanctions on Russia on Tuesday after Moscow’s recognition of two separatist regions in Ukraine as independent entities, with the United States set to unveil their own measures shortly.

Chief among their targets: Russian banks and their ability to operate internationally.

Yet the impact of the new sanctions is likely to be minimal. Western governments – for now – are preferring to keep the much larger sanctions packages that they have planned in reserve should the crisis escalate.

It means Russian bankers or their Western counterparts with exposures to the country won’t be losing much sleep.

Here’s how the banks are being targeted and which measures might hit harder:

WHAT HAS BEEN ANNOUNCED SO FAR?

European foreign ministers agreed to sanction 27 individuals and entities, including banks financing Russian decision-makers and operations in the breakaway territories.

The package of sanctions also includes all members of the lower house of the Russian parliament who voted in favour of the recognition of the breakaway regions.

Britain imposed sanctions on Gennady Timchenko and two other billionaires with close links to President Vladimir Putin, and on five banks – Rossiya, IS Bank, GenBank, Promsvyazbank and the Black Sea Bank.

The lenders are relatively small and only Promsvyazbank is on the Russian central bank’s list of systemically important credit institutions.

Bank Rossiya is already under U.S. sanctions from 2014 for its close ties to Kremlin officials.

Experts said the measures were modest.

“This is a limited, targeted start, a shot across the bows,” said Paul Feldberg, a sanctions expert and partner at law firm Jenner & Block, adding that Putin was unlikely to care.

The United States, which has drawn up a raft of measures to hit Russia’s economy should Moscow invade Ukraine, has yet to announce sanctions that will be imposed immediately but is set to later on Tuesday.

WHAT WILL THE IMPACT BE?

For now – minimal.

Russia’s large banks are deeply integrated into the global financial system, meaning sanctions on the biggest institutions could be felt far beyond its borders.

But the new sanctions focus on smaller lenders.

The measures targeting banks are not yet as extensive as those imposed after Russia’s annexation of Crimea in 2014, although many of those sanctions remain in place.

Then the West blacklisted specific individuals, sought to limit Russia’s state-owned financial institutions’ access to Western capital markets, targeted the bigger state lenders, and imposed widespread limits on the trade of technology.

Britain’s new measures refrained from imposing limits on the biggest state banks, cutting off capital for Russian companies, or ejecting other prominent so-called Russian oligarchs from Britain.

Shares in Russia’s biggest banks, Sberbank (SBER.MM) and VTB soared after the state-controlled groups escaped the sanctions.

Analysts say Russian institutions are better able to cope with limited sanctions than eight years earlier, and Russian state banks have cut their exposure to Western markets.

Russia has since 2014 diversified away from U.S. Treasuries and dollars – the euro and gold account for a bigger share of Russia’s reserves than do dollars, according to a January report from the Institute of International Finance.

Russia has some strong macroeconomic defences too, including abundant hard currency reserves of $635 billion, oil prices near $100 a barrel and a low debt-to-GDP ratio of 18% in 2021.

WHAT MIGHT COME NEXT?

The EU has said it is ready to impose “massive consequences” on Russia’s economy but has also cautioned that, given the EU’s close energy and trade ties to Russia, it wants to ratchet up sanctions in stages.

Officials consider Tuesday’s measures as a first round of sanctions.

Beyond lenders that do business directly with the breakaway regions, it’s not clear yet when or whether the EU will hit the biggest banks.

Washington has prepared a raft of measures including barring U.S. financial institutions from processing transactions for major Russian banks by cutting “correspondent” banking relationships, sources told Reuters last week.

Disabling international payments would hit hard.

Those measures, however, may be kept in reserve.

Washington could also wield its most powerful sanctioning tool against certain Russian individuals and companies by placing them on the Specially Designated Nationals (SDN) list, effectively kicking them out of the U.S. banking system.

Sources familiar with the planned measures said VTB Bank, Sberbank, VEB, and Gazprombank are possible targets, although it is unclear whether Russian banks would be added to the SDN list.

WHAT WOULD HIT HARDEST?

What the region’s banks and Western creditors fear most is that Russia is banned from a widely used global payment system, SWIFT, which is used by more than 11,000 financial institutions in over 200 countries.

Such a move would hit Russian banks hard but the consequences are complex – banning SWIFT would make it tough for European creditors to get their money back and Russia has been building up an alternative system to SWIFT.

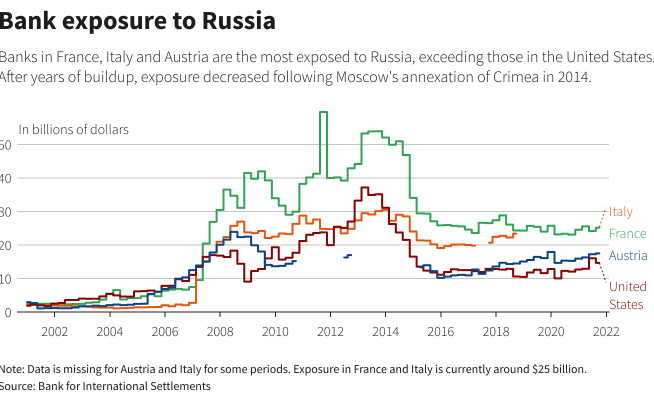

Data from the Bank of International Settlements (BIS) shows that European lenders hold the lion’s share of the nearly $30 billion in foreign banks’ exposure to Russia.

WHICH FOREIGN BANKS ARE MOST EXPOSED?

Europe’s banks – particularly those in Austria, Italy and France – are the world’s most exposed to Russia, and have been on high alert should governments impose new sanctions.

Italian and French banks each had outstanding claims of some $25 billion on Russia in the third quarter of 2021, according to BIS figures. Austrian banks had $17.5 billion. That compares with $14.7 billion for the United States.

Among the most exposed lenders is Austria’s RBI (RBIV.VI), which has big operations in Russia and Ukraine, and said “crisis plans” would come into effect if things deteriorate. Its shares closed down 7.5% on Tuesday.

Many foreign banks have, however, significantly reduced their exposure to Russia since 2014, making some bankers less concerned about the threat of sanctions.

Additional reporting by Tom Sims in Frankfurt and Iain Withers in London, Editing by Kevin Liffey and Rosalba O’Brien

Credit | Reuters